Inheritance Tax for British Expats

Hey, Brits! We bet “What’s the deal with Inheritance Tax (IHT)?” is a question that’s crossed your mind. If you’re looking to pass on assets or you’re on the receiving end, understanding IHT is undoubtedly key. We’re here to guide you through the essentials, and yes, the numbers as well. Ready? Read on below!

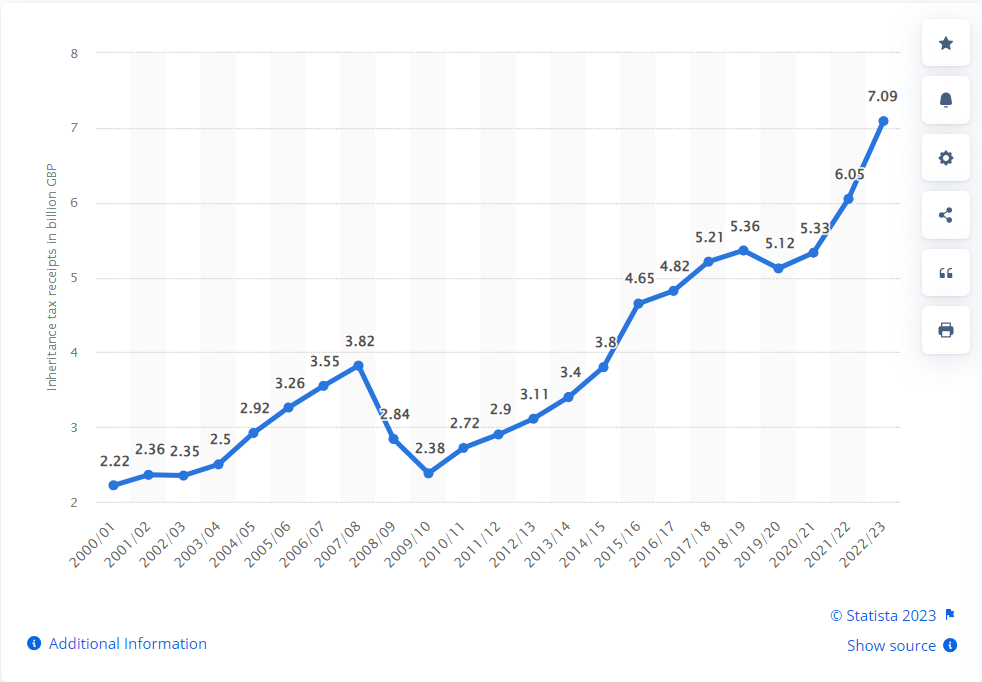

In the past decade, from 2012/13 to 2022/23, HMRC’s Inheritance Tax collections have seen a dramatic rise, surging by 128% from £3.11 billion to £7.09 billion, marking a somewhat startling increase of £3.98 billion. As property prices soar and the cost-of-living rises, more and more people find themselves falling into the IHT net. It’s not just a problem for the super-rich anymore.

Before we get onto how it affects us Brits abroad, what are the dreaded rates? For most people, the IHT rate is 40% on anything above that £325,000 threshold. However, if you leave at least 10% of your “net estate” to a charity, that rate drops to 36%.

Eligibility – who gets the bill?

So, who gets hit with IHT? If your estate – including property, money, and possessions – exceeds £325,000, the taxman could come knocking. But it’s not all doom and gloom. Spouses and civil partners can often pass assets to each other tax-free and may be able to increase that £325,000 limit.

Are you?

- Married with Kids: If you're married and have children, remember that your spouse inherits tax-free, and the first £325,000 of your estate goes to the kids without IHT.

- Single: With no spouse or civil partner, the whole estate could be taxed above the £325,000 limit. Be sure to have a will in place to dictate how you'd like things divvied up.

Inheritance Tax for Expats

In just three years, IHT collections have skyrocketed by 33%, reaching an all-time high of £7.09 billion in 2022-23.

If you’re living abroad, it’s easy to think you’re free from UK Inheritance Tax (IHT) obligations. Think again! Being an expat doesn’t exempt your UK assets from IHT, and depending on your domicile status, your entire worldwide estate could even be subject to UK IHT.

01

Establish Your Domicile Status

HMRC divides you into two categories: residency and domicile. While it’s easy to change your tax residency by moving abroad, losing your UK domicile status is a different story. Any form of ties to the UK, no matter how thin, can make you liable for UK tax.

02

Qualifying Non-UK Pension Scheme (QNUPS)

Contributions to approved overseas pensions like QNUPS can make your funds entirely exempt from IHT. Typically, they are in neutral jurisdictions such as Malta, Isle of Man and Gibraltar. However, this exemption is granted only if it’s a genuine retirement provision.

03

Discounted Gift Trust

Here, you can effectively gift money while retaining control over it. You can contribute without limit to the trust, nominating as many beneficiaries as you want. As its name suggests, there is an immediate discount or reduction in IHT liability. This percentage will vary with age and gender. The rest of the assets in the trust will still be liable to IHT but only for seven years, reducing each year – until the entire investment and its growth is completely exempt from IHT!

Oh, and one more thing – the original investor into the trust retains the right to withdraw an ‘income’ from the investment. This strategy is perfect for you who want to retain some control whilst working down that IHT bill that will be passed on to your loved ones.

04

Utilise Exemptions and Reliefs

Just like residents, expats can also benefit from Business Relief, Agricultural Relief, and the rules surrounding gifts. For example, any money or assets you gift more than seven years before your death could be exempt from IHT. More on this below.

Exemptions and Reliefs

Ok… how about some good news! There are specific circumstances that might give you relief from IHT, as follows:

- Business Relief:

This can be between 50% and 100% and reduces the value of a business or its assets when calculating IHT. For more information on how to claim business relief, see here.

- Agricultural Relief:

If you own qualifying agricultural property, you could see significant reductions in your IHT bill. For more information on Agricultural Relief, see here.

- Gifts:

The ‘7-year rule’ means any money or assets you gift more than seven years before your death could be exempt. The types of gifts that fall under this include money, household items, property, and even stocks and shares.

Here are some things to note about gifting:

- Spousal and Civil Partners Gifts: Gifts between spouses or civil partners are generally tax-free, providing that the recipient is a permanent UK resident and is legally connected to you.

- Charitable Donations: Contributions to charities or political parties won't be counted toward the value of your estate for Inheritance Tax purposes.

- Annual Allowance: Each tax year, you can gift up to £3,000 without it being included in your estate's value. You can also carry over any unused portion of this exemption to the next tax year, although this is only possible for one year.

- Small Gift Allowance: You're allowed to give multiple gifts of up to £250 per person in each tax year, but this can't be combined with any other allowances for the same person.

- Special Occasion Gifts: For weddings or civil partnerships, you can offer tax-free gifts up to certain limits based on your relationship with the recipient.

For an in-depth guide on how these exemptions can benefit you and your beneficiaries, click here.